You’re making loan payments every month and suddenly have extra cash — a bonus, a tax refund, maybe a side hustle payout. You wonder: should I throw this at my loan? And more importantly, how much will it actually save me?

That’s exactly what an EMI calculator with a prepayment option helps you figure out. It shows you your regular monthly payment and what happens when you pay extra — so you can make a confident, informed decision before moving a single dollar.

What Is an EMI Calculator with Prepayment Option?

EMI stands for Equated Monthly Installment. It’s the fixed monthly amount you pay toward a loan — part interest, part principal — until the loan is fully paid off.

A standard EMI calculator tells you what your monthly payment will be based on your loan amount, interest rate, and term. That’s useful. But it’s also pretty basic.

An EMI calculator with a prepayment option goes further. It lets you enter extra one-time or recurring payments on top of your regular EMI — and instantly shows you:

- How many months you’ll cut off your loan term

- How much interest you’ll save in total

- Your updated payoff date

- The revised remaining balance after each prepayment

This is the tool you want when you’re actually trying to get out of debt faster — not just know what you owe each month.

How EMI Is Calculated (The Formula Behind It)

You don’t need to memorize the formula, but understanding it helps you see why prepayments are so powerful.

The standard EMI formula is:

EMI = [P × r × (1 + r)^n] / [(1 + r)^n – 1]

Where:

- P = Principal loan amount

- r = Monthly interest rate (annual rate ÷ 12)

- n = Number of monthly payments (loan term in months)

Here’s a quick example. Say you take out a $25,000 auto loan from Wells Fargo at 6.5% annual interest for 60 months (5 years).

- Monthly rate = 6.5% ÷ 12 = 0.5417%

- EMI ≈ $489/month

- Total paid over 5 years = $29,340

- Total interest paid = $4,340

That $4,340 is just gone — you never see it again. Now let’s see what one prepayment does to that number.

Real-Life Prepayment Example (With Actual Numbers)

Let’s say it’s Month 6 and you get a $3,000 federal tax refund. You decide to put all of it toward your auto loan as a lump-sum prepayment.

Here’s what changes:

| Without Prepayment | With $3,000 Prepayment | |

| Remaining Term | 54 months | ~47 months |

| Total Interest | $4,340 | ~$3,190 |

| Interest Saved | — | ~$1,150 |

| Payoff Date | Month 60 | ~Month 53 |

You save over $1,100 in interest and get out of the loan 7 months early — just by directing one tax refund toward the principal.

That’s the real power of prepayment. And without a calculator to model this, most people just deposit that refund into checking and keep paying the regular installment for 5 years.

Try the EMI Calculator with Prepayment on behzadaslam.com

Types of Prepayments You Can Model

Not all prepayments look the same, and a good EMI calculator lets you model several types:

1. One-Time Lump Sum Prepayment

You make a single large extra payment at a specific point in the loan — like that tax refund or a work bonus. You pick the month, enter the amount, and see the revised schedule.

2. Recurring Monthly Prepayment

You decide to pay an extra $100 or $200 every month on top of your regular EMI. This is sometimes called “rounding up” your payment. It’s simple, consistent, and surprisingly effective over time.

3. Annual Prepayment

Common with mortgages — you make one extra payment per year, often equal to one full monthly installment. On a $400,000 30-year mortgage at 7%, doing this every year can shave off 5–6 years of payments.

4. Combination

Some calculators let you mix and match — a lump sum now, then recurring extras later. This mirrors real life the best.

When Does Prepayment Make the Most Sense?

Prepayment isn’t always the #1 move — it depends on your full financial picture. But here are the situations where it almost always makes sense:

Your interest rate is above 6–7%. If you’re carrying a personal loan 4]\’ vat 10–15% or a high-rate auto loan, every dollar toward principal is an immediate guaranteed return at that rate. No investment can reliably beat that risk-free.

You’re early in the loan term. In the first few years, the majority of your payment is going toward interest. Prepaying early shifts that curve dramatically.

You don’t have high-interest credit card debt. If you’re carrying $5,000 at 22% APR on a Chase or Bank of America card, pay that off first. Prepaying a 5% mortgage while carrying 22% credit card debt doesn’t make financial sense.

You have your emergency fund covered. The general rule in the US is 3–6 months of expenses in savings. Don’t drain that to prepay a loan — an unexpected job loss or medical bill will just push you back into debt.

Watch Out for Prepayment Penalties

Some lenders charge a prepayment penalty — a fee for paying off your loan early. This is more common in mortgages and personal loans than auto loans, though it varies by lender and state.

In the US, federal law limits prepayment penalties on Qualified Mortgages — generally, lenders can only charge them within the first 3 years of the loan, and the amounts are capped. Still, always check your loan documents or call your lender before making a large prepayment.

If your loan has a prepayment penalty, plug that cost into your EMI calculator’s savings estimate. You might still come out ahead — or you might decide to wait until the penalty period expires.

Using an EMI Prepayment Calculator for a US Mortgage

Mortgages are where prepayment math gets really interesting — and really impactful.

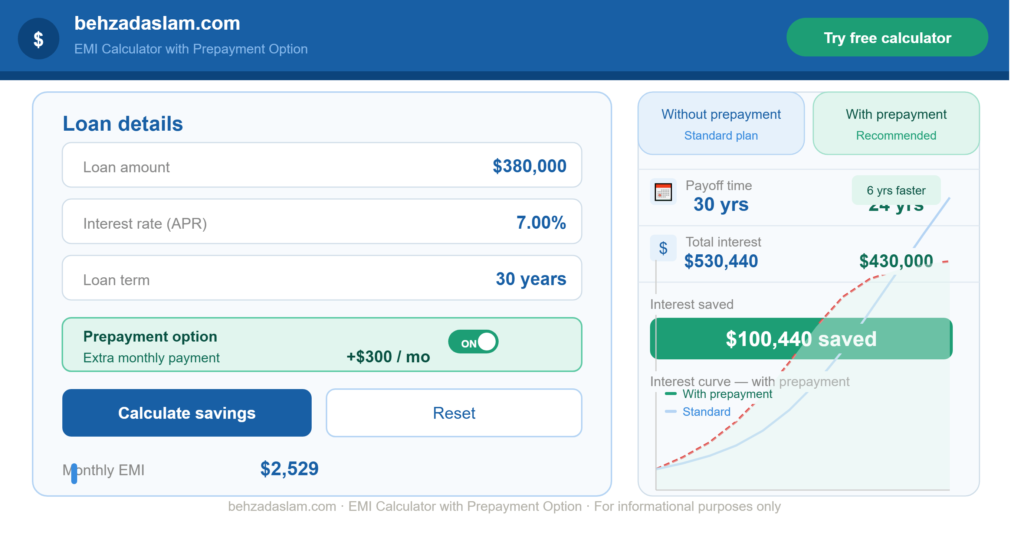

Imagine you bought a home and took out a $380,000 mortgage at 7.0% for 30 years with Bank of America.

- Monthly EMI ≈ $2,529

- Total paid over 30 years = $910,440

- Total interest = $530,440

That’s half a million dollars in interest. Now here’s what happens if you add just $300/month as a recurring prepayment:

- New payoff time: ~24 years (6 years early)

- Total interest paid: ~$430,000

- Interest saved: ~$100,000

Three hundred dollars a month — less than a car payment for many people — saves you six years and a hundred thousand dollars. That’s the kind of number that makes you want to log into your mortgage portal immediately.

EMI Calculator vs. Amortization Schedule — What’s the Difference?

People sometimes confuse these two, so it’s worth clearing up.

An amortization schedule shows you the complete month-by-month breakdown of every payment — how much goes to interest, how much to principal, and your remaining balance after each installment.

An EMI calculator computes your monthly payment and summarizes the totals.

An EMI calculator with prepayment does both — plus it recalculates everything dynamically when you add extra payments. It’s the most practical tool for actual debt planning, not just curiosity.

How to Use the EMI Prepayment Calculator on behzadaslam.com

It’s straightforward — here’s the quick process:

- Enter your loan amount — for example, $25,000 for an auto loan

- Enter the interest rate — say, 6.5% APR

- Enter the loan term — 60 months

- See your base EMI — the calculator shows your monthly payment instantly

- Add a prepayment — choose lump sum or recurring, enter the amount and timing

- Compare the results — see your new payoff date, revised total interest, and savings

No spreadsheets. No guesswork. Just clear numbers you can act on.

FAQ

Q: Does prepaying a loan affect my credit score?

Yes, but usually in a minor way. Paying off a loan early closes that account, which can slightly reduce your credit mix or average account age. For most people, the financial savings far outweigh any small, temporary credit score dip. Your US credit score (300–850 range) is unlikely to drop significantly from responsible early payoff.

Q: Is it better to prepay my mortgage or invest in my 401(k)?

This is a common dilemma. If your employer offers a 401(k) match, always contribute enough to get the full match first — that’s an instant 50–100% return. After that, compare your mortgage interest rate vs. expected investment returns. At a 7%+ mortgage rate, prepaying often makes more sense than investing in a taxable account. Under 4–5%, investing historically wins long-term.

Q: Can I make prepayments on a federal student loan?

Yes. Federal student loans allow prepayment without penalties. When you make extra payments, specify that they should be applied to the principal balance, not toward future payments. This reduces the interest that accrues over time.

Q: What’s the best time in a loan term to make a prepayment?

Earlier is almost always better. Because interest is front-loaded in standard amortizing loans, prepayments made in Year 1 or 2 save significantly more than the same payment made in Year 8. The EMI prepayment calculator will show you this clearly if you model two identical prepayments at different points in the timeline.

Wrapping Up

An EMI calculator with a prepayment option isn’t just a number-crunching tool — it’s a planning tool. It turns a vague question like “should I pay extra on my loan?” into a concrete answer with real dollar savings attached to it.

Whether you’re managing a $380,000 mortgage, a $25,000 auto loan, or a personal loan from your local credit union, knowing your prepayment impact before you commit is smart financial practice. The math is clear: the earlier you pay extra, the more you save.

Try the EMI Calculator with Prepayment Option on behzadaslam.com and see exactly how much your next extra payment could save you.

Open the EMI Prepayment Calculator

Disclaimer: This article is for informational purposes only. Please consult a certified financial advisor for personalized advice tailored to your financial situation.

Written by Behzad Aslam, Founder of behzadaslam.com