Your loan payment is eating into your budget every month, and you’re wondering if there’s a way to bring it down — without dragging out the loan for another five years.

Good news: yes, there is. And it doesn’t require refinancing into a 30-year mortgage or starting over.

You can reduce your monthly loan installment by lowering the principal balance, negotiating a better interest rate, or making a lump-sum prepayment — all while keeping your original payoff timeline intact. Here’s exactly how to do it, step by step.

Why You’d Want to Lower the Payment Without Extending the Term

Most people assume the only way to lower a monthly payment is to stretch the loan out longer. But extending tenure means paying more interest over time — sometimes tens of thousands of dollars more.

That’s a bad trade.

What you actually want is a lower payment and the same payoff date. Surprisingly, this is very achievable — especially if your credit score has improved, your home has gained equity, or you have some savings you can put to work.

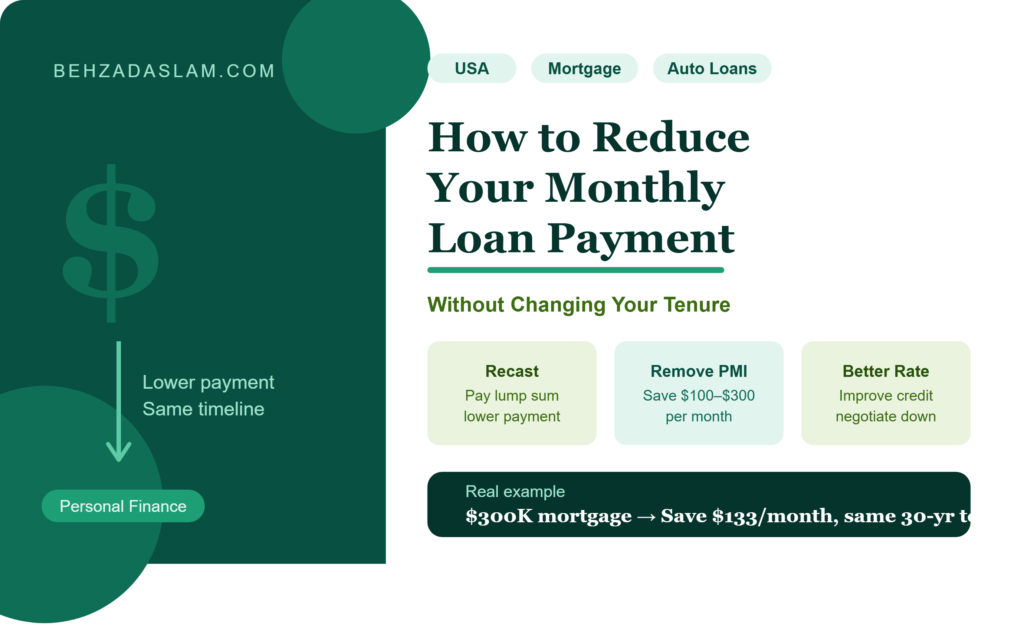

Method 1: Make a Lump-Sum Prepayment (Principal Reduction)

This is the most direct and powerful method.

When you make an extra payment toward your loan principal, the outstanding balance drops. Since your monthly payment is calculated on the remaining principal, your lender can recalculate — or “recast” — the payment at a lower amount, keeping the same term.

Real example:

Say you took out a $300,000 home mortgage at 7% interest over 30 years. Your monthly payment comes out to roughly $1,996.

Now suppose you get a $20,000 bonus and put it straight toward the principal. Your new balance is $280,000. If the lender recasts the loan, your new monthly payment drops to around $1,863 — saving you $133 every single month, for the same 30-year term.

That’s $1,596 back in your pocket every year, without touching the timeline.

👉 Try the Loan EMI Calculator on behzadaslam.com to run your own numbers

Most lenders, including Wells Fargo and Chase, allow principal prepayments. Just make sure you specify it’s going toward principal, not just “next month’s payment.”

Method 2: Mortgage Recasting (The Underused Strategy)

Most borrowers have never heard of recasting — which is a shame, because it’s incredibly effective.

Recasting means you pay a large chunk toward your loan principal, and the lender re-amortizes the loan over the remaining original term at the same interest rate. The result? A lower monthly payment without refinancing or changing the end date.

This is different from refinancing. There’s no credit check, no appraisal, and the fee is typically just $150–$300 — compared to closing costs of $5,000–$12,000 on a refinance.

Who offers recasting?

- Bank of America (conventional loans)

- Chase

- Wells Fargo

- Most major servicers for conventional mortgages

Note: FHA loans, VA loans, and USDA loans typically don’t qualify for recasting. If you’re on one of those, look at Method 3 or 4.

Method 3: Negotiate a Lower Interest Rate

If your credit score has improved since you took the loan, you have leverage.

The US credit score range is 300 to 850. If you borrowed when your score was 650 and it’s now sitting at 740+, you’re now in a much stronger position to negotiate — especially with auto loans or personal loans where terms are more flexible.

For auto loans specifically:

Call your lender and ask about rate modification. If they won’t budge, look at refinancing through a credit union. Credit unions like Navy Federal or Alliant often offer significantly lower rates than traditional banks, and refinancing an auto loan typically costs nothing in fees.

Dropping from 9.5% to 6.5% on a $35,000 auto loan over 60 months saves you about $50/month — and roughly $3,000 over the life of the loan.

For mortgages:

Negotiating down without refinancing is harder, but not impossible if you have a strong payment history and your lender values your business. You can also explore a loan modification if you’re experiencing hardship — many lenders offer this formally.

Method 4: Remove Private Mortgage Insurance (PMI)

If you have a conventional home loan, you might be paying PMI — and it’s probably costing you $100 to $300/month on top of your actual loan payment.

Here’s the thing: PMI is not permanent.

Once your home’s loan-to-value ratio drops to 80% or below, you’re legally entitled to request PMI removal under the Homeowners Protection Act. If your home’s value has gone up (which it likely has in recent years), you may have already crossed that threshold.

Request a new appraisal, submit the paperwork to your servicer, and that $150–$300/month disappears — without touching your loan term at all.

Method 5: Refinance Into a Lower Rate, Same Remaining Term

Okay, this one involves refinancing — but here’s the key distinction: you’re not extending the term.

If you have 22 years left on your mortgage, you refinance into a 22-year loan (not a new 30-year). This is a move most people don’t think to make because lenders default to pushing you toward 30-year products.

If rates have dropped even half a percent since you borrowed, this approach can cut your monthly payment meaningfully. At $400,000 remaining on a mortgage, the difference between 7.5% and 6.8% is about $180/month.

The catch: closing costs. Run the break-even math before you commit. If closing costs are $6,000 and you save $180/month, your break-even is around 33 months. If you plan to stay in the home past that, it makes sense.

👉 Use the Mortgage Refinance Calculator to check your break-even point

What Doesn’t Work (And Why People Get This Wrong)

A lot of people ask their lender to “just lower the payment” — and the lender obliges by extending the term. Suddenly your 15-year loan becomes a 20-year loan, and you end up paying $30,000 extra in interest.

That’s the lender’s version of a solution. Not yours.

Also: skipping payments, making late payments, or requesting a forbearance — these feel like relief but damage your credit score and often result in deferred interest being added to your balance. That’s the opposite of what you want.

Real-Life Scenario: How Sarah Lowered Her Car Payment by $88/Month

Sarah bought a used Toyota Camry in 2022 with a $28,000 auto loan at 10.4% (her credit was fair at 622 at the time).

By mid-2024, her score had climbed to 748. She refinanced through Alliant Credit Union at 6.1% — same remaining 42-month term. Her payment dropped from $597 to $509.

That’s $88/month back. No extended term. No extra interest paid over the life of the loan. Just a smarter rate, applied to the same window of time.

She used an auto loan calculator before making the call — and confirmed the numbers before committing to anything.

👉 Try the Auto Loan Calculator at behzadaslam.com

How to Know Which Method Is Right for You

| Situation | Best Approach |

| You have a lump sum of cash | Principal prepayment + Recasting |

| Your credit score improved | Refinance or rate negotiation |

| You’re paying PMI | Request PMI removal |

| You have a conventional mortgage | Recasting |

| You have an FHA/VA/USDA loan | Refinance into same-length term |

| Your lender won’t negotiate | Shop credit unions |

FAQ

Q: Can I reduce my mortgage EMI without refinancing?

Yes. The most effective way is mortgage recasting — make a large principal payment, pay a small admin fee ($150–$300), and your servicer re-amortizes your loan at a lower monthly payment. No credit check, no appraisal, no new loan.

Q: Does making extra loan payments reduce my monthly payment automatically?

Not automatically. Extra payments reduce your balance and save you interest, but your servicer won’t lower the monthly amount unless you formally request a recast. Contact your lender after making the prepayment and ask them to recalculate.

Q: Will removing PMI affect my loan term or interest rate?

No. PMI removal has zero effect on your loan term or rate. It simply removes a monthly insurance charge that was tacked on because your initial down payment was under 20%.

Q: Is it better to refinance or recast?

Depends on the situation. Recasting is cheaper and faster but doesn’t change your rate. Refinancing makes more sense when rates have dropped significantly since you borrowed — but factor in closing costs before deciding.

Wrapping Up

A lower monthly payment doesn’t have to mean a longer loan. Between principal prepayments, recasting, PMI removal, credit score-based rate renegotiation, and smart refinancing into a same-length term — there are real, proven ways to bring that number down without handing the bank more years of your income.

The key is knowing which strategy fits your loan type and financial situation. Run the numbers first — always.

👉 Ready to see what your new payment could look like? Try the free EMI and Loan Calculator at behzadaslam.com and find out in seconds.

Disclaimer: This article is for informational purposes only. Please consult a certified financial advisor for personalized advice tailored to your situation.

Written by Behzad Aslam, Founder of behzadaslam.com